By Subrata Majumder

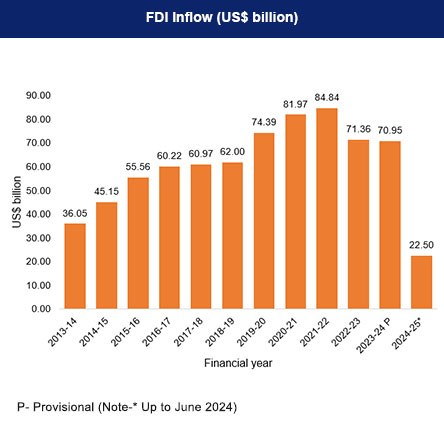

An introspection of foreign direct investment flow in India reveals that FDI fell on the lowest ebb in 2023-24 within 5 years. This is despite the fact that country achieved one of the highest growth in the economy. It dropped to US$ 44,423 million in 2023-24, from US $ 59,636 million in 2020-21. This is in contrast to spur in GDP growth, viz, 9.4 per cent in 2021-22, 6.7 percent in 2022-23 and 7.2 percent in 2023-24.

The anomaly between FDI growth and GDP raised eyebrows. This highlighted that developing nations like India, who are dependent on FDI for economic development, became vulnerable to global investment flows.

India is under utter disappointment, as to why FDI did not align with the growth in the economy, despite being wooed by factors , like rising resilience to global oil shock after shifting to Russian oil, overcoming crucial COVID 19 epidemic and enlarging the domestic market due to spur in GDP growth and demographic advantages.

These demonstrate that FDI growth has seen a dramatic change in the world since past three years. Hitherto, the growth of global FDI has been aligning with GVC (global value chain) . Nearly, one third of global FDI was flowing in GVC and China has been one of the biggest receivers of FDI.

With the end of COVID 19 and increase in geopolitical tensions, the link between FDI flow and GVC was disrupted. According to a UNTACTD report, entitled “Global economic factoring and shifting investment pattern” the growth of FDI and GVC were no longer aligned with GDP and trading growth.”

The report said, “since 2010, global GDP and trade have grown annually by an average of 3.4 percent and 4.2 percent respectively, even during rising tensions”. But, FDI growth in manufacturing stagnated near to zero, the report said.

The report outlined factors for lagging FDI were investors’ increasing caution due to shift in international production and GVC, rising protectionism and geopolitical tensions.

UNTACTD report highlighted 5 factors for change in the strategy of FDI flow. They were increase in prominence in service sector, rise in geopolitical tensions, rise in investment in environment technologies, focus on high tech sectors and low preference to less developed countries.

UNTACTD report unveiled that strategic changes in global FDI embraces a major shift in FDI flow to service sector from manufacturing. From 2004 to 2023, the share of cross-border FDI in green field projects in service sectors leaped from 66 percent to 81 percent.

In contrast, FDI in manufacturing stagnated for two decades, before experiencing a significant downturn. Eventually, the global strategic changes in FDI had a major impact on India. Since past three years (2021-22 to 2023-24) computer software/ hardware (mainly software) was the biggest recipient of FDI, followed by service sector. Together with service sector, these non-manufacturing sectors accounted for one-third of total FDI flow in India (32.4 percent in 2023-24).

In contrary, FDI in manufacturing dwindled during these three years. For instance, FDI in automobile, which was the third biggest sector in 2021 -2022, accounting for 11.2 percent in the total FDI, slipped to 3.4 percent in 2023-24.

Generally, volume of FDI flow depends upon manufacturing and non-manufacturing sectors. This is because computer software and service sectors (excepting infrastructure) are small size projects in respect of investment. Service sectors, which mainly include banking, insurance and other non-banking sectors, are widely different from the point of view of size of investment. Banking and insurance are big size investment projects. But, there were few cases of FDI in banking and insurance, due to stringent regulations in India.

Recent global conflicts, like Russia-Ukraine war, sanctions on Russia and prolonged China-India tiff disrupted usual investment pattern. This caused unstable investment relationship and limited chances for strategic diversifications, UNTACTD report said.

For India, growing tension between India-China limited the scope for foreign investors in China to diversify to India under China+1 strategy. Investment by USA is a case in point. USA was the second biggest foreign investor in India in 2020-21. It was US$ 13,823 million. It plunged to US $ 4998 million in 2023-24 – a drop by over 63 percent. In contrast, USA investment in ASEAN surged by over 112 percent in 2023 over 2021, Presumably, this demonstrates that USA investors in China preferred to shift to ASEAN than in India under China+1 strategy.

Given the growing concerns over climate changes in the world, “FDI in environment technologies, like wind and solar energy, emerged the fastest growing sectors, outside service sectors”, the UNTACTD report noted. For instance, it said that FDI in electrical vehicles and batteries soared by 61 percent in 2020 to 171 percent in 2023.

India lagged in the field of environment technologies. In manufacturing of electrical vehicles and batteries, it is at the stage of infancy. At present, it produced merely 0.9 million electrical cars in 2023-24, as compared to 4.9 million petrol/diesel passenger cars in the country. This demonstrates that India is yet to pick up the demand for electrical vehicles in the country. This swayed away India from the new strategic shift in global FDI.

According to UNTACTD report “Global investment flows increasingly favour sectors in developed and emerging markets”.

India, though an emerging economy and is aiming to emerge as the 3rd largest economy by the end of this decade, could not attract attention of global investors yet. India is yet to enter semiconductor device manufacturing club in the world, despite being 2nd biggest manufacturer of mobile phones.

Therefore, it is the global change in FDI strategy, which dumped FDI flow in India. Focuses on shifting from manufacturing to service sectors and environment technologies kept the foreign investors distant from investing in India. Eventually, India’s policy initiatives to attract FDI, such as PLI scheme (Production Linked Initiative), and shifting India as supply chain hub of the world, did not augur well for the foreign investors. (IPA Service)

India-China Agreement On LAC On October 21 Is A Welcome Development

India-China Agreement On LAC On October 21 Is A Welcome Development