NEW DELHI: The Organisation of the Petroleum Exporting Countries’ (Opec) outlook for global crude oil demand in 2024 is beginning to show signs of caution. After months of holding steady, the cartel has revised its projections for the second consecutive time, reflecting the uncertainty surrounding key economic players.

Opec reduced its global crude oil demand forecast for 2024 for the second month in a row in its September Oil Market Report, released on September 10.

The group had initially maintained its original 2024 forecast, first released in July 2023. However, in August, it adjusted the projection downward from 2.25 million barrels per day (bpd) to 2.11 million bpd. In the September report, the forecast has been further lowered to 2.03 million bpd, though this remains significantly higher than estimates from the International Energy Agency (IEA) and the US Energy Information Administration (EIA).

The August revision was based on real data from the first two quarters of this year and concerns over slowing economic growth in China. However, the September report downplays these concerns, noting that China’s economic growth “is expected to remain well supported.” The report also highlights that stronger growth forecasts for India, Russia, and Brazil are likely to compensate for any further slowdown in China.

Earlier this year, the IEA revised its forecast for global oil demand growth for this year, anticipating an increase of 1.1 million bpd, a reduction of 140,000 bpd from its previous estimate.

This downward adjustment was largely attributed to sluggish demand in advanced economies, particularly those within the Organisation for Economic Co-operation and Development (OECD). The IEA highlighted weaker industrial activity and an unusually mild winter as factors curbing gas oil consumption, especially in Europe, where the declining prevalence of diesel vehicles has already led to reduced demand.

The difference between the forecasts of Opec and IEA, amounting to 0.93 million bpd, underscores the widening divide between these key institutions.

Earlier in the year, Reuters reported a similar divergence, with the gap between their February projections standing at 1.03 million bpd—the largest disparity since at least 2008.

The IEA lowered its supply growth forecast for 2024, citing significant production outages in Brazil and logistical bottlenecks in the US. According to the agency, global oil supply will increase by 580,000 bpd this year, bringing total production to a record high of 102.7 million bpd. This is a downward revision from last month’s forecast of a 770,000 bpd increase.

These supply-demand dynamics are expected to play a crucial role in Opec+ decision-making as the group, which includes Opec members and allies such as Russia, considers whether to extend voluntary production cuts into the latter half of the year. The IEA estimates that the demand for Opec+ crude, along with inventories, will average 41.9 million bpd in 2024, a slight uptick from the previous month’s estimate of 41.8 million bpd, suggesting a tighter market overall.

While Opec recently expressed optimism about the global economy, the IEA took a more cautious stance, noting that despite some improvement since late last year, inflationary pressures in key Western economies are likely to weigh on oil demand. Elevated borrowing costs in both the US and Europe are hampering economic growth, the IEA added, further tempering oil demand.

For 2025, the two organisations have slightly more aligned expectations than before, yet the divergence remains significant. The IEA has raised its demand growth estimate to 1.2 million bpd, while Opec has kept its forecast steady at 1.85 million bpd.

The IEA and Opec not only differ in their short-term projections but also diverge sharply in their long-term outlooks. The IEA expects global oil demand to peak by 2030 as the shift towards cleaner energy sources gains momentum. Conversely, Opec remains more bullish, projecting that demand will continue to grow until at least 2045, with emerging economies leading the charge and resistance to net-zero policies slowing the transition.

The IEA, originally established to ensure energy security for industrialised nations, has shifted its focus in recent years towards advocating for renewable energy and climate change mitigation. This has led some Opec members, notably Saudi Arabia’s Energy Minister Prince Abdulaziz bin Salman, to question the agency’s impartiality, accusing it of moving from forecasting to political advocacy.

IEA member countries, primarily energy consumers, are pushing for rapid renewable energy adoption to accelerate the shift towards a low-carbon economy. On the other hand, Opec members, who depend heavily on fossil fuel revenues, are concerned about the economic impact of a hasty transition away from oil.

Both organisations frequently revise their oil demand forecasts, as predicting global economic trends and energy consumption is inherently complex. The IEA has adjusted its 2024 growth forecast upwards for the past three months, reflecting a projected 50 per cent decline in growth, partly due to the increasing adoption of electric vehicles (EVs).

A Reuters analysis of forecast revisions between 2008 and 2023 found that the IEA underestimated demand 56 per cent of the time, while Opec did so 50 per cent of the time. Despite this, the minimal discrepancy between the two makes it difficult to determine which organisation has been more accurate over the long term. So, it is quite possible that both agencies may be way off in their demand forecasts, although it seems unlikely because the ‘save earth’ initiatives across the globe have shifted realities for fossil fuel consumption as a whole.

In recent months, falling oil prices have prompted speculation about how Opec might respond. The group had planned to increase oil supply in October, but a steep drop in crude prices has led some members to reconsider. Both Brent and WTI crude benchmarks have declined by around 5 per cent this week, hitting their lowest levels since December. Weak demand data from major economies, including China and the US, have been the primary drivers of this price drop, overshadowing supply disruptions in Libya.

Opec has been limiting oil production since 2022 through a mix of production cuts and voluntary reductions. However, internal pressures are building, as smaller members express frustration with these self-imposed limitations, especially following the voluntary production cuts of 2.2 million bpd introduced at the end of 2023. This growing dissatisfaction, which even led Angola to exit the group in January, could push Opec to begin unwinding the cuts later this year.

China’s flagging property market has been a significant factor in the decline of national crude oil demand, which fell to 16.6 million bpd in May, its lowest level since mid-2022. Refineries worldwide are also experiencing shrinking margins—the difference between crude and product prices—which, along with rising global crude inventories, points to potential future weakness in crude prices.

Even Opec’s September report attributed the revision to factors stating, “headwinds in the real estate sector and the increasing penetration of LNG trucks and electric vehicles are likely to weigh on diesel and gasoline demand going forward.”

China’s electric vehicle (EV) market has grown substantially, thanks to generous government subsidies and incentives. In a historic achievement in July, sales of EVs and hybrids in China surpassed those of internal combustion engine vehicles for the first time. The China Passenger Car Association (CPCA) reported that new energy vehicles, which include EVs and hybrids, accounted for 51.1 per cent of all passenger vehicle sales that month. EV and hybrid sales rose by 37 per cent year-on-year to 878,000 units in July, while sales of traditional vehicles dropped 26 per cent to 840,000 units.

Meanwhile, the European Union (EU) has seen substantial growth in wind and solar power generation, with capacity expanding 65 per cent since 2019. This increase displaced about one-fifth of the EU’s fossil fuel generation, according to a report by think tank Ember. Wind and solar energy now contribute 44 per cent of the EU’s total electricity mix, up from 34 per cent in 2019. The corresponding decline in coal and gas generation has reduced the share of fossil fuels in the EU’s electricity production to 32.5 per cent from 39 per cent.

The rapid growth of renewable energy in Europe, combined with similar trends in China, highlights the accelerating global shift away from fossil fuels—further complicating the outlook for global oil demand in the coming years.

Source: Business Standard

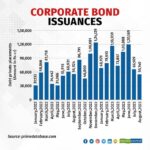

Corporate Bond Issuances Fall 22 Per Cent In August As Firms Await Fed Rate Cut

Corporate Bond Issuances Fall 22 Per Cent In August As Firms Await Fed Rate Cut