By K R Sudhaman

India may not have crossed the US$4 trillion economy mark as some of the Narendra Modi fans tried to propagate in the recent days in social media but certainly the total GDP is approaching that level. However some economists fear that GDP growth in the last few quarters may be overestimated. With wholesale price index being in negative territory during the last 2 or 3 quarters, growth is bound to be overestimated as WPI is used as a deflator in the calculation of growth numbers. So the GDP growth at 7.8 per cent in the first quarter this financial year 2023-24 is believed to be grossly exaggerated, so also the GDP numbers of the previous quarters. So according to one estimate the actual growth during the period under review could at best be around 6.5 per cent.

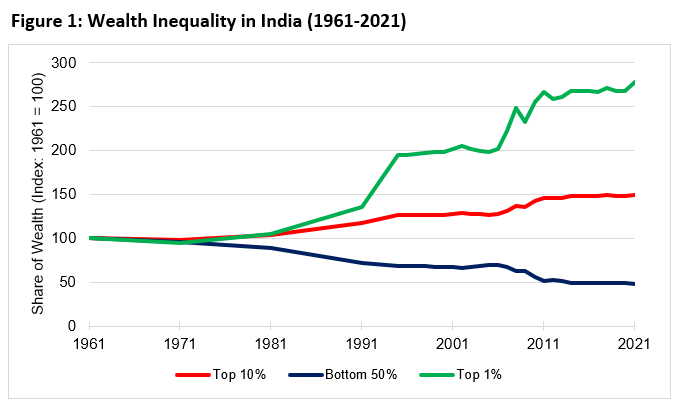

Of course $ 4 trillion economy is just a number, so also projection of $ 5 trillion in the next couple of years or for that matter $7 trillion by 2030, unless there is visible improvement in the quality of life of vast majority of the people. Otherwise it will only promote crony capitalism, jobless growth, rural distress and pushing more people below poverty line. Growth is certainly important for poverty alleviation but the quality of growth is equally important to ensure more and more people to come out of poverty. Also skilling the youth and providing them quality and employable education to enable them stand on their own feet are equally important if India were to take advantage of the so called demographic dividend. Unfortunately that is not happening in a manner it ought to be because of wrong policies and communal politics, apart from blatant and shameless corruption widespread in the political system.

Finance Minister Nirmala Sitharaman and RBI Governor Shaktikanta Das have rightly flagged two important issues – high domestic debt and sticky inflation. These are critical macroeconomic issues and any widening of these cracks could threaten stability, which meant monetary and fiscal actions that could derail the growth momentum. Added to it, are worrying numbers on unemployment put out by CMIE lately. The unemployment has gone beyond 10 per cent again from 6-7 per cent, which is should cause concern. The latest monthly economic review of finance ministry has flagged inflation as one of the persistent downside risks to the economy. Even though there are some positive developments in the economy, yet downside risks persisted. “Inflation is one of them that has kept the government and RBI on alert,” it said.

Strangely this observation has come at a time when retail inflation based on the consumer price index (CPI) dropped to 4.9 per cent in October from 5 per cent in September, mainly because of cheaper non-food and non-fuel products. However food inflation remained at the same level in October. The central bank has cautioned that food prices may push inflation. The continued Russia-Ukraine war coupled with Israel-Hamas stand-off do not augur well for the global economy. These uncertainties have already started pushing global crude oil prices besides impacting global trade. Apart from increased global commodity prices, India’s merchandise exports growth are slowing down. The FDI flow into India, too has been impacted, though not at a worrying level.

The government may claim India has become 5th largest economy from 10th position during Modi era. It had overtaken Britain to become fifth largest economy and it will overtake Germany and Japan in a couple of years to become third largest economy. India’s growth certainly improve in coming years. But common man is not amused with these figures as a large number of wage earners have lost their jobs. The doubling of allocation to MNREGA programmes from the budgeted level so far this year itself is a clear indication that jobs are not available to them. This also amounted to fudging of figures as proposing lower allocation for MNREGA programmes while presenting the budget in February this year, the finance minister has shown a lower fiscal deficit than the actual number.

Princeton economist Ashoka Mody has claimed that the country’s Gross Domestic Product during April-June quarter of 2023-24, would come to 4.5 per cent instead of 7.8 per cent as National Statistical Office takes into account only estimates of domestic income and not expenditure to calculate growth figures. Chief economic advisor, V Anantha Nageswaran rejected this claim saying that the government has been consistent in its method for calculating the growth numbers.

But there is some merit in former chief economic advisor Arvind Subramanian in saying growth is overestimated because of using WPI as deflator. Former chief statistician Pronab Sen agrees with the view point and expected the real growth to be around 6.5 per cent instead of 7.8 per cent as official figures indicate in the first quarter of this financial year. He however points out it’s a double edged weapon. When WPI is in negative territory, certainly there could be overestimation of growth, but when WPI is high and in double-digits, there is underestimation of growth numbers. This problem arises when WPI is used as deflator.

What one needs to worry now is how to create more jobs. At least 11 million jobs have to be created every year to absorb people getting into the job market. That apart, the job market has to absorb many who have been pushed into self-employment to keep themselves afloat, especially after closure of large number MSME units during Covid. There was also migrant labour issue due to lockdown. There is one positive sign lately that MSME is slowly reviving in the last one or two quarters if one goes by improved lending to the sector.

In sum, there are several pressing issues to be addressed in the economy. Just being carried away by growth numbers will serve no purpose. In fact the 6-7 per cent growth that Indian economy has been striving at is not enough to provide the jobs that is required to absorb the people getting into the job market. According to former RBI governor Raghuram Rajan, India need to get back to 8-9 per cent growth to take advantage of the demographic dividend. (IPA Service)

On Israel’s Gaza War, Hindutva Forces In India Are In Cahoots With Zionists

On Israel’s Gaza War, Hindutva Forces In India Are In Cahoots With Zionists