By Kunal Bose

China has cement capacity of around 3.5bn tonnes (source China Cement Big Data Research Institute) in which the industry leader China National Building Material (CNBM) Group alone has a share of 515m tonnes while the second largest player Anhui Conch has capacity of around 370m tonnes. Combination of excess capacity, price weakness resulting from demand squeeze in the real estate sector, unhealthy competition and fall in profit margins have kept the condition ideal for mergers and acquisitions leading to consolidation of Chinese cement industry. Then there is constant nudge from Beijing, worried about cement’s share in carbon emissions and economic burden that overcapacity entails, for deep capacity reorganisation. CNBM, a state undertaking, that itself merged into it another public sector unit China National Materials Group in 2016, is undergoing deep reorganisation for some time going beyond cement to rearrangement of production equipment development and manufacturing operations.

CNBM chairman Zhou Yuxian says the Group being the industry leader it has the responsibility of becoming the role model in addressing the problem of national cement overcapacity. In the meantime, to counter setback in domestic cement sales and profits, CNBM is doing two other things besides cement reorganisation: (i) Beefing up international business, including exploring opportunities that may be available in China’s much trumpeted Belt & Road infrastructure programme. (ii) Expand new materials business that includes carbon fibre, glass fibre and materials for lithium-ion batteries. The industry’s No. 2 Anhui Conch Cement must have bought over a dozen cement companies since 2022 and it still remains in hunt for more. BBMG, the third in the pecking order is also a participant in capacity consolidation. “What is happening in cement by way of capacity consolidation and reorganisation is a reflection of what Beijing has done with steel, but with greater force and success,” says an industry observer.

There is consensus among analysts that the combination of continued distress of the real estate sector and the likely slower growth in infrastructure development to be caused by difficult fund allotment condition at the province level based on falling revenues from land sales will continue to hurt cement makers in the current year. In this context, Fitch Ratings says: “Chinese cement demand likely to remain weak in 2024 due to distress in the property sector, but producers’ margins may stabilise… We expect cement capacity in China to decrease in 2024, driven by exits of smaller, unprofitable producers. In the medium term, the government’s policy on capacity control and decarbonisation of the sector will further reduce capacity.” Cement makers took a hit as China’s real estate development fell 10% year-on-year to $1.53 trillion in 2023.

CNBM chairman has described the past year as one of “storms and challenges” when the industry saw its profits eroded by as much as 50% to $4.42bn, the lowest since the mid-2000s. As for CNBM Group, the 2023 revenue fall was 10% to $29bn while profits suffered a 52% setback to $534m. All this could not have been otherwise since the industry, according to CNBM president Wei Rushan, had to endure “insufficient demand, weakening expectations and weakening off-peak season characteristics.”

Moreover, the twin problems of surpluses with demand flattening and high costs remained. Revenue rises of Anhui Conch were on account of growth in trading activities but sales of cement were down. In a weak price situation, company profits nosedived 33% to $1.48bn. Expectedly, smaller companies in general fared badly in terms of sales volume and profits. The 2024 outlook for the industry is not encouraging either with cement prices refusing to move north. In fact, cement prices in China during the final week of March were down nearly 1% compared identical period in 2023.

The situation is already bad. But, according to CCA, this will become worse if there is a “price war, either nationally or regionally.” It wants the industry to accept that the “new normal” is cement demand fall on the back of slowdown in infrastructure development. A way has to be found to resolve the supply side problem and that requires production discipline and excess capacity shedding. The industry already has manufacturing presence overseas by way of ownership of cement mills and CCA says cement companies should further explore opportunities abroad for growth. In the meantime, China’s National Bureau of Statistics has released data of cement production in 2023, which fell 4.5% to 2.02bn tonnes from 2.11bn tonne in 2022. China cement production may stabilise around 2bn tonnes, but that also will leave surpluses in the system having a bearish impact on prices.

What is not to be missed is that 2023 saw a slower rate of output fall compared to the 10.4% decline in 2022 over 2021. In spite of production fall, China accounts for nearly half of 2023 global cement output of 4.1bn tonnes. India and Vietnam are the next two largest cement producers in the world. The woes of Chinese property sector by way of home price falls, bloated debts and slow new starts has unavoidably spilled over to cement companies. The worst sufferer in the process is the Hong Kong listed China Tianrui Group Cement with production capacity close to 60m tonnes, which on April 10 found its market capitalisation fell 99% in one swoop forcing the stock exchange to suspend trading.

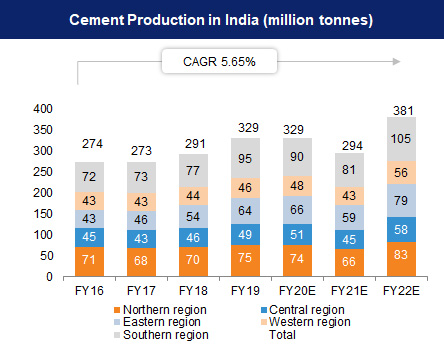

In sharp contrast to the Chinese scene, the Indian industry in expansion mode commissioned 119m tonne new capacity in the past five years to make a total of 595m tonnes, says RK Sharma, director general of Federation of Mineral Industries. This is not all. As Crisil says, the Indian industry is to add another 150-160m tonne capacity over the next five years. “The growth through both organic and inorganic routes is to meet demand surge for the binding material from the housing and infrastructure sectors.” There is also the competition among industry leaders to wrest a bigger share of the growing market by having more capacity.

According to Crisil, large groups are likely to commission up to 55% of new capacity. Even while there is weakening of cement prices in recent months, Crisil is hopeful that in spite of the “largest in a decade” capacity expansion, “cement prices are expected to stay stable with utilisation rate in 70% to 75% range.” Some industry officials, however, say privately a fallout of aggressive capacity expansion will be “intense competition” among producing companies in most markets denying them the option to raise prices. To add to their difficulties, cement demand from the real estate sector, accounting for 55% of total use of the commodity, has remained weak. No wonder, the average Indian cement price fell by 1% in 2023-24. Impact of the price fall was, however, largely negated by raw materials (coal and pet coke) prices decline and higher sales volume.

The forward looking cement industry in Europe where capacity is largely concentrated but where also exist several medium and small sized independent units remains at the forefront of using cutting-edge technology, says Sharma. The industry there is projected to grow at a CAGR of 1.9% between 2023 and 2028 to reach a volume of 202.83m tonnes. The growth, according to Dublin based research group Research & Markets, will happen on the back of rising construction and infrastructure activities across Europe. In elaboration, it says as the European Union remains committed to strengthening all infrastructure segments from transportation to water management and every country in the region is expanding residential, including affordable housing and non-residential commercial construction, cement demand will get a boost. Another report says, the continent’s cement industry registered a CAGR of 2.1% between 2018 and 2022 and attained a volume of 181.17m tonnes.

At the same time, European cement users are showing a distinct preference for green cement for use in eco-friendly structures to bring down harmful emission, says Sharma. Emphasis on manufacturing green cement is largely because of growing pressure from environmentalist groups and user community committed to sustainable construction practices. Green cement is made from waste materials such as recycled concrete, slag, quarrying and mining waste and power plant refuses. Besides environmental consideration, green cement is finding increasing use in Europe as it is found to have better “crack and corrosion resistance, freezing and thawing resistance, sulphate attack resistance and minimal chloride permeability” than conventional cement. Cement has the unenviable reputation of being among the worst polluters. The industry is responsible for emitting approximately 7% of annual global greenhouse emissions. The prime reason is cement production is overly dependent on coal-fired electricity. Each tonne of cement produced using such power typically releases 0.6 tonne of carbon in the air.

Cement’s environment disturbing quotient further increases because of high levels of pollution associated with limestone mining. In the available circumstances, the European industry is setting the example for the rest in the world by raising the use of renewable biofuels, install carbon capture and storage (CCS) and reuse waste heat to generate electricity. Now as part of decarbonisation of cement making, Holcim has begun the use of hydrogen as an alternative fuel. In fact, cement makers both in China and India taking the lead from their European counterparts are doing things to become carbon neutral at some point.

To cite a specific example, China’s Anhui Conch is following the path of Holcim in using more and more biomass fuel to progressive lower emissions involved in cement making. The company’s first biomass plant commissioned in late 2020 with capacity to extract energy from 300,000 tonnes of plant material a year. When run on full capacity, the plant will make use of 75,000 tonnes of coal redundant, thereby eliminating 200,000 tonnes of carbon emissions. Anhui Conch, which has a target to cut emission density by 6% over five years to 2025 is now building a larger biomass plant.

The UK based consulting IA Cement has forecast a US demand rise of around 3% in the current year as a “challenging housing market is expected to be offset by volumes from the $1.5 trillion infrastructure bill ramp up, with spending peaking in the period 2024-26.” Housing starts in the US have remained muted with mortgage rates staying high and the existing house owners are not to give up the advantage of purchases made earlier with low-cost mortgages, says Sharma. The US industry, with 2022 capacity of 119m tonnes and a further 6.2m tonnes from grinding units, found its clinker production dipping to about 77m tonnes from 80m tonnes a year before. Capacity fell more than 7m tonnes in 2020. Underutilisation of capacity has grown in the face of consumption rising steadily over a decade to 120m tonnes in 2023. The trade is showing a distinct preference for competitively priced cement of foreign origin.

Cement demand in Latin America in 2024 present a mixed bag, with consumption likely to improve modestly. Mexico and Brazil will see demand growing while the November election victory for the TV celebrity turned politician Javier Milei has catapulted South America’s second-largest economy Argentina into an unpredictable future. Economic uncertainty will inevitably have a negative bearing on Argentinian cement demand. In the meantime, high rates of inflation in Colombia has forced the central bank to peg interest rates uncommonly high. This, however, restricts housing demand and construction (including government funded infrastructure building) activities paring cement demand.

Blessed with rich deposits of limestone, countries in the Middle East and North Africa have built large cement making capacity, but now with overcapacity and pressure on prices dogging the industry. The two leading producers in the region are Egypt (2022 production 92m tonnes) and Saudi Arabia (85m tonnes). The next in the pegging order is UAE with 45m tonne production. The combined capacity of MENA region was 430m tonnes. Saudi Arabia leads in cement use (62m tonnes), followed by Egypt (50m tonnes), Iraq (31m tonnes) and Algeria (24m tonnes). What does the oversupply scene forebode for the region: First, price war among producers will continue for long limiting their income and second, the smaller producing countries will find it extremely challenging to build new capacity. (IPA Service)

…Concluded.

The writer is a leading economic journalist of the country.

Supreme Court’s Interim Order May Not Be Implemented By Two BJP State Govt’s On Ground

Supreme Court’s Interim Order May Not Be Implemented By Two BJP State Govt’s On Ground