By Anjan Roy

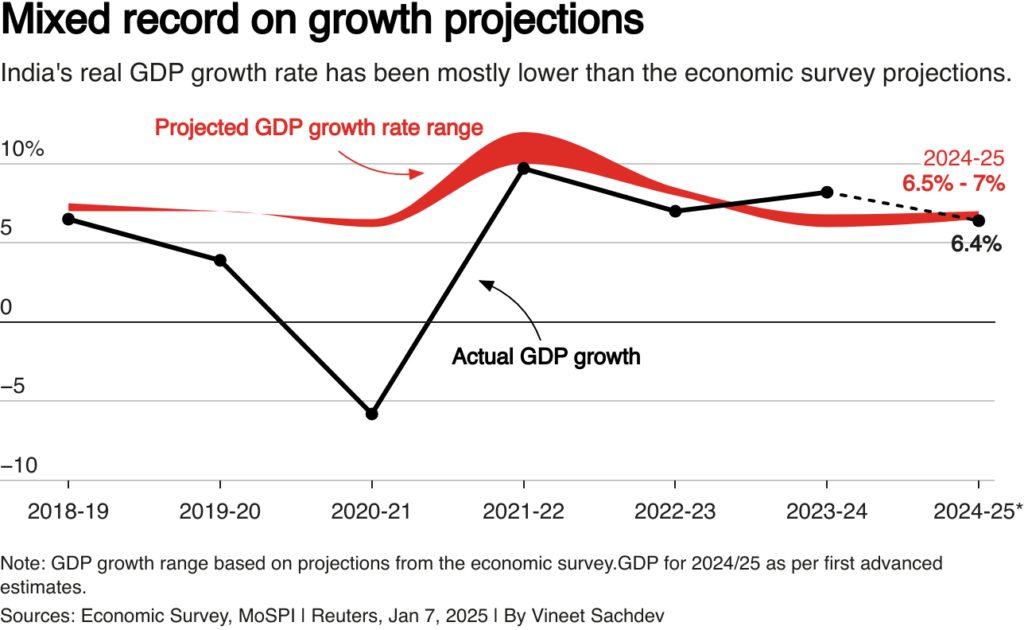

No sooner than the latest GDP advanced estimates were released, doomsday sayers have stated with settled conviction that India has slowed down and should not claw back into the 8%-plus performance bracket in the next few years. Theirs view is that India might remain in the 6%-6.5% level for the foreseeable future.

Let us look at the facts a little closer. India had clocked a 8.2% growth in 2023-24. The latest release show a print of 6.4% for 2024-25. This is a sharp fall from the heights of post-Covid period when the maximum growth rate had peaked to 9.7% in 2021-22. In the past thirteen years since 2012-13, growth rate exceeded 8% in four years.

Going by the trends, India’s GDP grew by 7% in most years on average and the economy has the potential to grow by over 7% a year, provided that unprecedented developments do not interfere with its functioning. These include force majeure developments like a global pandemic or a man-made crisis — one like a bout of demonetisation.

If anything, the Indian economy has been traditionally hamstrung by government interference and obnoxious ideas of control and restraint from the government agencies.

Having seen the constraints, for a major economy to grow at a natural pace, without too much of artificial boosters, at 7%-plus is no mean achievement. The growth mania should not generate an expectation of an overmuch trajectory with lots of boosters. Instead, it should be allowed to grow at its own pace at an optimum speed.

The growth mania had gripped the policy wonks and casual observers both periodically and at critical moments. It was during the prime ministership of Rajiv Gandhi when such a frenzied debate broke out in the run up to the preparation of the seventh quinquennial plan. The Planning Commission was debating internally and was divided in two camps.

Dr Raja Chelliah, member, and one of the most renowned economists of his time, had advocated a more cautious approach and advised growth target to be pegged at a moderate, more achievable level. Another camp in the commission, spearheaded by the flamboyant, Abid Hussain, a former commerce secretary and high profile public intellectual, suggested the plan to be a set at a very ambitious pitch.

Dr Chelliah’s point was that an overambitious plan straining the capacities of the economy could boomerang and hurt the prospects of growth itself.

Abid Hussain’s pitch on the controversy was pithy, saying that all windows of the economy should be opened clear to allow fresh breeze to come in. In the process if some flies enter, let it. We will tackle the problems accordingly.

When the ripples of the Planning Commission debate reached the ears of the prime minister, he had disdainfully commented about the Planning Commission members, specifically the more conservative ones. He said, “the planning Commission is packed with a bunch of jokers”. Prime minister was young and impatient. But the comment was not much appreciated.

What is important is not growth per se. But the quality of the growth and its spread and how far it could be sustained without straining at the seams. Overheating of the economy leading to hitting the capacities in sectors could result in distortions and inflation. These could harm the longer term prospects.

But looking at the latest disaggregated figures, it is clear that the sudden drop in the overall growth stemmed from the steep deceleration in the secondary sector. GVA at constant prices slipped sharply from 9.7% in 2023-24 to 6.5% in 2024-25 for the secondary sector. The secondary sector accounts for a quarter of the overall GDP and its growth shrinkage would naturally affect the overall performance of the economy.

Focussing even more on the tertiary sector, it is mainly the industrial economy, has decelerated sharply. Manufacturing growth rate, for example, has halved over the latest period from around 10% in 2023-24 to just around 5% in 2024-25. Again if we look at the performance of the three sectors of the economy over the five year period we see the primary sector has grown at lower rates but has been most stable. It is the secondary sector, that is, manufacturing, electricity generation, which have fluctuated widely in terms of annual growth.

Along with this, the tertiary sector, which has emerged over the years as the lynch pinch for the performance of the economy, accounting for 55% of the GVA, had also slipped albeit marginally. However, a more buoyant performance of the tertiary sector could have compensated for the loss of steam in the secondary sector.

Focussing further into the disaggregated figures of the segments of the economy, the four major segments included in the Index of Industrial Production, IIP, namely, mining, manufacturing, electricity generation and metallic minerals, have all slipped in the period under reporting. But these have been rather the recurrent themes of the GDP trends. That shows the need for correction and maybe some policy interventions or ay least a look for the inherent causes.

It is possible that by concentrating attention on correction of the inhibiting factors for these segments of the economy we should be able to give a more sustained boost to the overall performance.

Looking at the figures from the other side, that is, expenditure we notice that private final consumption, which remains the prime growth engine for the Indian economy, has shown vigorous trends. Private final consumption expenditure at constant prices has jumped substantially from 4% in 2023-24 to 7.3% in the latest year. Public sector consumption, that is, government expenditure, has also risen. That is, the internal demand situation remains buoyant.

But there is one but of concern on this side as well. Gross fixed capital formation has shrunk decisively from 9% in 2023-24 to 6.4% in 2024-25. This is what the total volume of investment in the economy. When investments slows down, there could be overall deceleration. A good part of this is however linked to the performance of the industrial economy, including the manufacturing, mining as well as construction. Thus, the policy directions from the latest figures, as well as, the trends revealed in the time series data shows there is clear need for some major boosts for the industrial economy.

If these GDP figures are what the union budget should seek to build upon, then the budget should do some introspection. In late January, the general profile of the union budget must have been already laid out. Still, the authorities must have had an inkling of what was coming. The budget should work out some framework for further encouraging the industrial sector. Obviously, the PLI schemes and other sops, have not been very successful in encouraging industrial growth in the economy. We need some rethinking. (IPA Service)

Latest UGC Draft Regulation Is A Direct Attack On The Principles Of Federalism

Latest UGC Draft Regulation Is A Direct Attack On The Principles Of Federalism